Over 60s private health insurance is one of the most googled financial questions among UK retirees right now. With NHS waiting lists stretched beyond 7 million, the idea of faster, private treatment is genuinely appealing. But health insurance for over 60s isn’t cheap, it doesn’t cover everything, and on a pension income it’s a serious monthly commitment. So is insurance for over 60s UK really worth it?

I spent 15 years as a mortgage broker before retiring. I know how financial products are sold — and how important it is to read past the brochure. This is my honest UK 2026 guide to costs, cover and how to choose — everything you need before committing to over60s health insurance.

How Much Does Over 60s Private Health Insurance Cost in the UK?

Age is the single biggest factor in the cost of over 60s private health insurance. The national UK average is around £80 per month, but for those in their 60s and 70s the figures are considerably higher — and they rise at renewal every year. Here’s a 2026 guide to typical costs and cover:

| Age | Basic | Mid-range | Comprehensive |

| Age 60 | ~£65/month | ~£90/month | ~£130/month |

| Age 65 | ~£80/month | ~£110/month | ~£155/month |

| Age 70 | ~£100/month | ~£140/month | ~£200+/month |

| Age 75 | ~£125/month | ~£175/month | ~£240+/month |

Premiums depend on postcode, health history, chosen insurer, and excess. London runs 20% higher. A comprehensive policy by your 70s can cost £2,400+ per year. See myTribe’s independent 2026 cost research for a full breakdown.

What Does Private Health Insurance for the Over 60s Actually Cover?

Before buying, it’s essential to understand what health insurance cover you’re actually getting — and what’s excluded. The health insurance cover available through over60s health insurance products varies significantly between insurers. Most people focus on the benefits and miss the small print.

What over 60s medical insurance typically covers:

- Consultant appointments and specialist referrals

- Diagnostic tests: MRI, CT and PET scans

- Inpatient surgery — hip replacements, cataracts, hernia repairs

- Cancer treatment, including some drugs not yet available on the NHS

- Cardiac investigations and treatment

What this type of cover does NOT include:

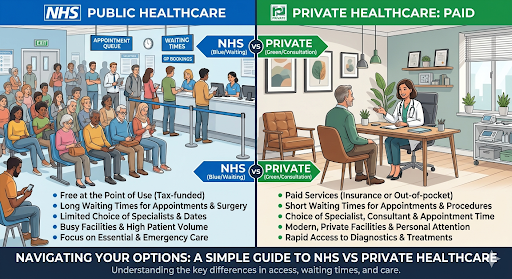

- A&E and emergency treatment — always NHS

- Long-term chronic conditions: diabetes, asthma, arthritis, high blood pressure

- GP appointments, routine dental and optical care

The key distinction is acute vs chronic. Over 60s private health insurance covers conditions that respond to treatment and resolve. For long-term chronic conditions, the NHS continues to provide that care.

Pre-Existing Conditions: The Biggest Trap in Over 60s Private Health Insurance

| ⚠️ Most People Miss This Over 60s private health insurance does NOT cover conditions you had before you took out the policy. Most people join hoping for quicker treatment for something they’re already dealing with — only to find it’s excluded from day one. |

Most policies use Moratorium Underwriting — automatically excluding conditions from the past five years. Exclusions can lift after two symptom-free years. Full Medical Underwriting declares everything upfront for more certainty at claim time.

5 Ways to Cut the Cost of Over 60s Private Health Insurance

Costs, cover and how to choose wisely — these are the three things that matter most. Here are five practical ways to pay less without losing the health insurance cover that counts:

- Increase your excess to £500+ — saves 20–40% on premiums

- Choose the 6-Week Wait Option — use the NHS if they can treat you within 6 weeks, saving 20–30%

- Opt for a limited hospital list — excluding London hospitals saves 15–25%

- Pay annually rather than monthly — saves 5–10%

- Use the guided consultant option — accept the insurer’s recommended specialist and save around 20%

Which Health Insurance Companies for Seniors Are Worth Considering?

Not all over60s health insurance products are equal. Here’s who to look at:

- Saga — exclusively for over-50s, AXA-backed, simplified claims process. The most tailored health insurance for over60s on the market.

- Bupa — benchmark for comprehensive cover, particularly strong on cancer care

- WPA — highest customer service scores, flexible cover options

- The Exeter — best for complex health histories and pre-existing conditions

- Aviva — good value, strong digital tools

Always compare quotes from health insurance companies for seniors via an independent FCA-authorised broker such as Drewberry Insurance rather than going direct to one insurer. And verify any insurer at the FCA Register.

Is Over 60s Private Health Insurance Worth It? My Honest Verdict

Medical insurance in retirement makes sense if you have a specific health concern where waiting time affects your quality of life, you can sustain the premiums long-term as costs rise each year, and you have realistic expectations about what’s covered.

It’s also worth considering as early retirement health insurance — taking out a policy in your early 60s while you’re relatively healthy locks in lower premiums and a cleaner health history for underwriting.

If you’re on a modest pension income, consider the hybrid approach first: a single private consultation (£200–£300) can bypass the referral wait and get you back on the NHS treatment queue faster, without a monthly premium commitment.

For more on staying healthy and financially protected in retirement, visit our Health & Wellbeing section or read our guide to free NHS health checks you’re entitled to.

Frequently Asked Questions

Can I get over 60s private health insurance with pre-existing conditions?

Yes, but they’ll almost certainly be excluded initially. Most over 60s private health insurance uses moratorium underwriting, automatically excluding conditions from the past five years. Exclusions can lift after two symptom-free years. Use full medical underwriting if you want certainty upfront.

How much does health insurance for over 60s cost per month?

A mid-range policy for a 65-year-old non-smoker outside London typically costs £110/month in 2026. Basic inpatient-only cover starts around £80/month. Comprehensive cover exceeds £155/month. Costs vary by postcode, health history, and excess chosen.

Is insurance for over 60s UK the same as NHS cover?

No. Insurance for over 60s UK works alongside the NHS, not instead of it. You keep all NHS rights. Private cover is used for planned treatment — surgery, diagnostics, consultants — while the NHS handles emergencies and chronic condition management.

What is the 6-Week Wait Option on over 60s health cover?

The 6-Week Wait Option on over 60s private health insurance means the insurer pays for private treatment only if the NHS wait exceeds six weeks. If the NHS treats you within six weeks, you use the NHS. This significantly reduces premiums — by 20–30% — and is ideal if your concern is very long waits rather than all waits.

How much is private health insurance for over 60s?

Costs depend on age, health history, and cover level. A 60-year-old in good health typically pays £90–£130 per month for mid-range cover, rising to £155+ by their late 60s and £200+ into their 70s. Shopping around at renewal every year is essential.

Which health insurance is best for a 60 year old?

Bupa, AXA Health, and Vitality are consistently rated highly for over 60s. Always compare on what is excluded rather than just the monthly premium — pre-existing condition terms vary significantly between insurers.

How much is Bupa for a 70 year old?

Bupa premiums for a 70 year old start from around £200 per month for basic cover. Costs rise at each annual renewal, so always compare alternatives before accepting your renewal quote.

What benefits do you get when turning 60?

Free prescriptions in Wales, potential Pension Credit eligibility, and discounted travel. Note that health insurance cover costs rise from age 60, so reviewing your policy beforehand is worthwhile.

Your Over 60s Private Health Insurance Checklist

- Check which conditions would be excluded under moratorium underwriting

- Set a budget that’s sustainable for the next 10 years, not just today

- Ask about the 6-Week Wait Option to reduce your premium by 20–30%

- Compare at least three quotes via an independent FCA-authorised broker

- Consider early retirement health insurance — the earlier you start, the lower your premium

- Never accept a renewal quote without shopping around

Sources

- The King’s Fund — NHS Waiting Times

- Which? — Best Private Health Insurance UK

- Health & Wellbeing — Honest Pensioner

Disclosure: This article contains links to third-party insurance comparison services. Honest Pensioner may receive a small commission if you obtain a quote through these links, at no extra cost to you. All editorial opinions are independent. This article is for information only and does not constitute financial advice. Always seek independent financial advice before purchasing any insurance product.