Cant pay my credit card this month? You are not alone — and you do have options. Across the UK, millions of people on fixed and limited incomes are asking exactly this question. This guide sets out 7 proven steps to help you take back control, without panic and without jargon.

If you can’t pay your credit card on a pension, a fixed income, or reduced earnings, the situation can feel impossible. But it rarely is. The earlier you act, the more choices you have.

| A Word From Our Editor — Mark Aucamp |

| During my 15 years as a mortgage consultant and my three years as a Debt Mangement advisor, I regularly sat with people over 55 who couldn’t pay their credit card bills on a limited pension income. The same story came up time and again — a balance that started small, quietly grew, and was now causing real distress. If you cant pay your credit card right now, this guide is written for you. |

Outstanding credit card debt in the UK hit £76 billion in 2025 — up 6.6% in a single year. Average credit card interest rates now sit at 24.65%. For anyone on a fixed income, that interest compounds fast. Nearly one in five over-65s cant pay credit card bills of around £3,500 from unexpected bills alone — that figure is 286% more than the average single pensioner’s monthly income of £906.

Car repairs, home repairs, and helping adult children with their own financial difficulties are the three most common triggers. If any of those sound familiar, read on.

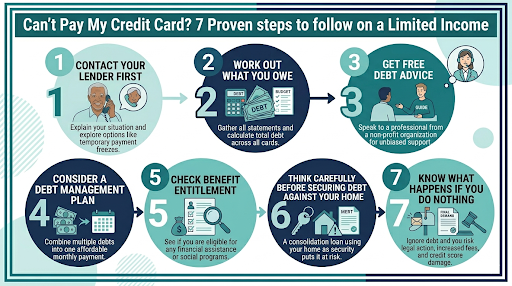

The 7 Proven Steps to Follow When You Cant Pay Your Credit Card

Step 1: Dont Ignore It — Contact Your Lender First

If you cant pay your credit card bill, the worst thing you can do is ignore it. Missed payments trigger late fees, damage your credit score, and can lead to a default or County Court Judgment (CCJ). Contact yourcredit card company before you miss a payment if at all possible.

Explain your situation honestly. Under FCA rules, lenders must treat customers in financial difficulty fairly. Most will offer one or more of the following:

- A temporary payment holiday of up to three months

- A reduced minimum payment plan

- A freeze on interest and charges

- A breathing space arrangement

Always ask for any arrangement to be confirmed in writing.

Step 2: Work Out Exactly What You Owe

If you cant pay your credit card debts then speak to any adviser, write out your complete financial picture. List every card, every balance, the minimum payment, and the interest rate on each. It feels daunting — do it anyway. You cannot tackle credit card debt without knowing the full size of it.

Split your debts into two columns:

- Priority debts — mortgage or rent, council tax, energy bills, court fines. These come first, always.

- Non-priority debts — credit cards, personal loans, catalogues, overdrafts.

Credit card debt is non-priority. That doesn’t mean ignore it — but your roof and your heating come first.

Step 3: Get Free Debt Advice — It Changes Everything

If you cant pay your credit card and feel overwhelmed, free professional debt advice is available right now. You do not need to pay anyone. The best debt help in the UK is completely free.

| Free Debt Help — Use These First |

| StepChange Debt Charity — Online debt advice available 24/7. Helped over 700,000 people in 2025. |

| Citizens Advice — Free advice in person, online or by phone. Over 400,000 debt cases in 2025. |

| National Debtline — Free telephone and online debt advice. |

| MoneyHelper — Government-backed guidance including a free Debt Advice Locator tool. |

| Age UK — Specialist debt advice for older people including a free benefits check. |

Step 4: Consider a Debt Management Plan

A Debt Management Plan (DMP) lets you make one affordable monthly payment instead of several. A free debt charity negotiates with your creditors on your behalf, and interest is often frozen. If you cant pay your credit card at the current rate, a DMP can give you real breathing space.

Key benefits:

- One single monthly payment you can actually afford

- Creditors often agree to freeze interest and charges

- No court involvement required

- Arranged completely free through StepChange or Citizens Advice

Step 5: Check Your Benefit Entitlement

Before accepting any debt arrangement, make sure you are receiving every penny you are entitled to. Many people on a limited income who cant pay their credit card are also missing out on benefits that could change their situation entirely.

If you are over State Pension age, check whether you qualify for:

- Pension Credit — worth an average of £3,900 a year, yet claimed by only 63% of those eligible

- Attendance Allowance — if you have a health condition or disability

- Council Tax Reduction

- Warm Home Discount and Cold Weather Payments

Call Age UK on 0800 678 1602 for a free benefits check. Even a modest increase in weekly income can make cant pay my credit card a problem of the past.

Step 6: Think Very Carefully Before Securing Debt Against Your Home

| A True Story — Details Changed to Protect Privacy |

| During my years as a mortgage consultant, I visited a gentleman whose wife had recently passed away. He lived in the large family home they had shared for decades. He was exploring options — equity release among them. |

| As we talked, the real picture emerged. Years earlier, he had allowed his only son to place a legal charge on the property to cover the son’s debts. Now, with those debts pressing, the son felt the time had come to sell. This grieving widower — in his most vulnerable moment — was facing losing the family home, not through his own decisions, but through a kindness shown to his child years before. |

| When I asked why he had not considered downsizing sooner, the answer was the same I heard dozens of times: he wanted to stay in his own home for as long as possible. My response was always the same — the decision could be made for you. |

| The country is quietly full of these stories, long before the current cost of living crisis. Read our guide to pension scams targeting older homeowners to understand the risks further. |

If you cant pay your credit card and someone suggests a secured loan, equity release, or a charge against your property — stop. Take independent legal and financial advice first. Once your home secures an unsecured debt, you have fundamentally changed your risk. Visit MoneyHelper’s guide on using your pension to pay off debt before making any decision involving your assets.

Step 7: Know What Happens If You Do Nothing

If you cant pay my credit card bills and take no action at all, here is the likely sequence:

- Missed payments trigger late fees and a note on your credit file

- After several missed payments the account defaults — this stays on your file for six years

- The lender may sell the debt to a collection agency

- In serious cases a County Court Judgment (CCJ) can be issued

- In extreme cases bailiffs can be involved — though this is rare for credit card debt alone

None of this is inevitable. Every step above can be stopped by taking action earlier. The sooner you act, the more options you have.

Your Questions Answered

What will I do if I cant pay my credit card?

If you cant pay your credit card, contact your lender straight away and explain your situation. Ask about a payment holiday, reduced payments, or an interest freeze. Then get in touch with StepChange or Citizens Advice for free, independent advice on your next steps.

What happens if you cant pay your credit card?

Missing a payment triggers a late fee and a mark on your credit file. Continued missed payments lead to a default, which stays on your file for six years. A County Court Judgment can follow in serious cases. Acting early gives you the most options — and the most control.

What if I am unable to pay my credit card on a limited income?

Being unable to pay your credit card debt on a limited income is more common than you might think. Free debt advice from StepChange, Citizens Advice or National Debtline can help you explore a Debt Management Plan, payment arrangements, and whether additional benefit entitlements could ease the pressure. Also see our guide to making a will in retirement — important reading if debt is affecting your wider financial planning.

How do I get rid of a credit card I cant pay?

Options include negotiating a reduced settlement with your lender, entering a free Debt Management Plan, or in serious cases an Individual Voluntary Arrangement (IVA). A free debt adviser will recommend the right solution for your circumstances. Never pay a fee for this advice — it is all available free of charge.

| Key Takeaways |

| Contact your lender before you miss a payment — FCA rules mean they must treat you fairly |

| Always prioritise rent, council tax and energy bills before credit card payments |

| Free debt advice from StepChange, Citizens Advice and National Debtline is available 24/7 |

| A Debt Management Plan can reduce your monthly payments to an affordable level |

| Check your benefit entitlement — unclaimed Pension Credit alone averages £3,900 a year |

| Never secure unsecured debt against your home without independent legal advice first |

| Acting early gives you the most options — ignoring the problem reduces them |

If a family member shared this article with you, or you are worried about an adult son or daughter struggling with debt, read our companion guide: My Child Can’t Pay Their Credit Card — How Can I Help? [COMING SOON]

Written by Mark Aucamp, Editor — Honest Pensioner | honestpensioner.com

Mark has 15 years of mortgage and consumer finance experience as former owner of Regional Finance Services.