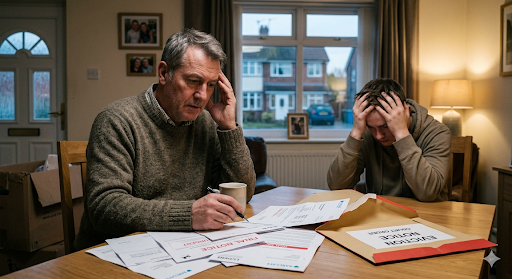

Son in debt and struggling to cope, you are not alone. Across the UK, thousands of parents over 55 are watching their adult children drown in credit card bills, loans and mounting financial pressure — and desperately wondering what they can do to help, many of the parents are on a limited income and not in a good place to help a son in debt.

When your adult children have financial problems, the instinct is to step in immediately. But before you do anything — hand over savings, remortgage your home, or offer to clear the debt outright — there are 5 essential things every parent should understand first.

| A Word From Our Editor — Mark Aucamp |

| In my 15 years as a mortgage consultant, I sat regularly with parents over 55 whose son or daughter were in debt. They came to me looking for solutions — equity release, secured loans, remortgages. The same pattern repeated itself time and again. This guide is written to share what I witnessed, and what I wish more parents had known before they acted. |

When You have a Son in Debt — A Pattern I Witnessed Many Times

During my years as a mortgage consultant, I regularly saw what happens when our children have financial difficulties and parents feel compelled to help. Three situations came up again and again:

- Parents taking out secured loans against their own home to clear a son or daughter’s debt

- Parents remortgaging to help an adult child onto the property ladder — only for that child to fall into debt shortly afterwards.

- Parents placing their home at risk by allowing a charge to be placed on it to secure their child’s borrowing

In every case, when I asked why they hadn’t considered downsizing or protecting their own finances first, the answer was the same. They wanted to help. They wanted to stay in their own home. And they trusted their child completely.

The problem is that when your son is in debt and or your daughter, the pressure mounts, even the best intentions can lead to decisions that put everything you have worked for at risk.

5 Essential Ways to Help When Your Son is in Debt

1. Listen First — Before You Offer Money

When your son is in debt, the first and most important thing you can do is listen without judgement. Find out the full picture before offering anything financial. How much does he owe? Who does he owe it to? Has he sought free debt advice?

Many parents hand over money before understanding the scale of the problem — only to find the debt returns within months because the underlying behaviour hasn’t changed.

Encourage him to contact StepChange Debt Charity or Citizens Advice for free, professional debt advice before any family money changes hands.

2. Help Him Understand His Options — Without Taking Them On Yourself

When children have financial problems, parents often feel responsible. You are not. Your role is to guide, not to absorb the debt yourself.

Sit down together and look at what free options exist:

- Debt Management Plans — one affordable monthly payment, interest often frozen

- Individual Voluntary Arrangements — a formal agreement with creditors

- Payment holidays — many lenders offer these under FCA rules

- Budgeting support — free from National Debtline and MoneyHelper

Visit MoneyHelper together — it has clear, impartial guidance on every debt option available.

3. Check Whether He is Claiming Everything He is Entitled To

Before assuming the only solution is family money, check whether you help your child by pointing him toward benefits and entitlements he may be missing.

Depending on his circumstances, he may be entitled to:

- Universal Credit — if his income has fallen

- Council Tax Reduction

- Discretionary Housing Payments

- Local welfare assistance schemes

Use the free benefits calculator at EntitledTo to check his entitlements before offering financial help. Even a modest increase in his income could make his debt manageable without you needing to step in at all.

4. If You Do Help Financially — Set Clear Boundaries

If after careful thought you decide to help your son in debt with money, do it with clear boundaries in place. This protects both of you.

- Agree whether it is a gift or a loan — and put it in writing

- Never give more than you can genuinely afford to lose

- Do not dip into your pension or retirement savings

- Seek independent legal advice if any property is involved

Also see our companion article: Can’t Pay My Credit Card? 7 Free Steps on a Limited Income — useful reading to share directly with your son or daughter.

5. Never Risk Your Own Home — The Decision Could Be Made For You

| A True Story — Details Changed to Protect Privacy |

| During my years as a mortgage consultant, I visited a gentleman whose wife had recently passed away. He lived alone in a large, substantial house — the family home they had shared for decades. He had come to me exploring his options. |

| As we talked, the real picture emerged. Years earlier, in an act of love and trust, he had allowed his only son to place a legal charge on the property to secure the son’s mounting debts. Now, with those debts pressing and no other solution in sight, the son felt the time had come to sell. |

| This grieving widower — in the most vulnerable period of his life — was facing losing the family home. Not through any decision of his own, but through a kindness he had shown his only child years before. |

| When I asked why he had never considered downsizing, his answer was the one I heard dozens of times in my career. He wanted to stay in his own home for as long as possible. My response was always the same: |

| ‘The decision could be made for you in the future.’ |

| The country is quietly full of these stories — long before the current cost of living crisis. Man and his castle. Until the castle is no longer his. |

If your son is in debt and someone suggests you secure a loan against your home, release equity, or allow a charge to be placed on your property — STOP. Take independent legal and financial advice before signing anything.

Read our guide to pension scams targeting pensioners to understand how unscrupulous firms target parents in exactly this situation. And before making any decisions involving your assets, visit MoneyHelper’s debt advice guidance.

Your Questions Answered

How do I help my son get out of debt?

Start by encouraging your son in debt to seek free professional advice from StepChange or Citizens Advice before any family money is involved. Help him understand his options — a Debt Management Plan, payment holiday, or benefits check may resolve the situation without you needing to step in financially.

Should I tell my adult children how much money I have?

This is a deeply personal decision. However, when your adult children have financial problems, being open about your own financial limits can actually protect both of you. If your son or daughter knows you have limited means, it removes the pressure — spoken or unspoken — for you to step in beyond what is safe for your own retirement.

What to do if my son is in debt and asking for help?

Listen carefully before acting. Find out the full scale of the debt, whether free advice has been sought, and what options already exist. Then decide what — if anything — you can safely offer without risking your own financial security. Never put your home or pension at risk for a child with debt without taking independent legal advice first.

How can I help my son clear his debt without risking my home?

If you want to help financially, consider a modest cash gift rather than anything involving your property. Never allow a charge on your home, never act as guarantor without understanding the full legal implications, and always take independent advice. Free guidance is available from Citizens Advice and MoneyHelper.

| Key Takeaways for Parents |

| Listen and understand the full picture before offering any financial help |

| Encourage your son or daughter to get free debt advice from StepChange or Citizens Advice first |

| Check whether your adult child is claiming all benefits they are entitled to |

| If you help financially, set clear written boundaries and never give more than you can afford to lose |

| Never allow a charge on your home or risk your pension without independent legal advice |

| The decision to sell or downsize is far better made on your own terms — before it is made for you |

If you are also worried about your own credit card debt on a fixed income, read our guide: Can’t Pay My Credit Card? 7 Free Steps on a Limited Income

Written by Mark Aucamp, Editor — Honest Pensioner | honestpensioner.com . Mark has 15 years of mortgage and consumer finance experience as former owner of Regional Finance Services.