Dreaming of spending your retirement years in the Spanish sunshine, the warmth of Cyprus, or closer to family in Australia? You are not alone. Each year, thousands of UK pensioners pack their bags and head overseas. But before you book that one-way flight, there is one thing you absolutely must understand about your uk state pension overseas — the rules are far more complicated than most people realise, and getting them wrong could cost you thousands of pounds over the course of your retirement.

In this article, we set out 5 important truths about your UK state pension overseas — covering frozen pensions, the major 2026 National Insurance changes, tax implications, and exactly what you need to do before you move. Whether you are already living abroad or just starting to plan, this guide is for you.

| ✅ Quick Summary — What You Need to Know |

| 1. You can receive your UK State Pension in almost any country in the world 2. But annual increases depend entirely on where you live — many countries get a frozen pension 3. From April 2026, voluntary NI contributions for expats became significantly more expensive 4. Tax treaties vary by country — you may pay tax in two countries without proper planning 5. You must notify both the DWP and HMRC before you move |

Truth 1: You Can Claim Your UK State Pension Almost Anywhere in the World

The good news first. You can claim your UK state pension overseas in the vast majority of countries worldwide. As long as you have paid enough National Insurance contributions — at least 10 qualifying years to receive anything, and 35 qualifying years for the full amount — your entitlement travels with you.

The full new State Pension for 2026/27 is £241.30 per week. You can check your own forecast and how many qualifying years you have by visiting the UK Government’s Check Your State Pension tool — you will need a Government Gateway login.

Payments can be made every 4 or 13 weeks directly into your overseas bank account, or into a UK bank account if you prefer. However, if you are paid in a foreign currency, exchange rate fluctuations can affect how much you actually receive — something worth factoring into your retirement income planning.

For more detail on how the State Pension is calculated, read our guide: State Pension Age Increases — What Every Pensioner Needs to Know.

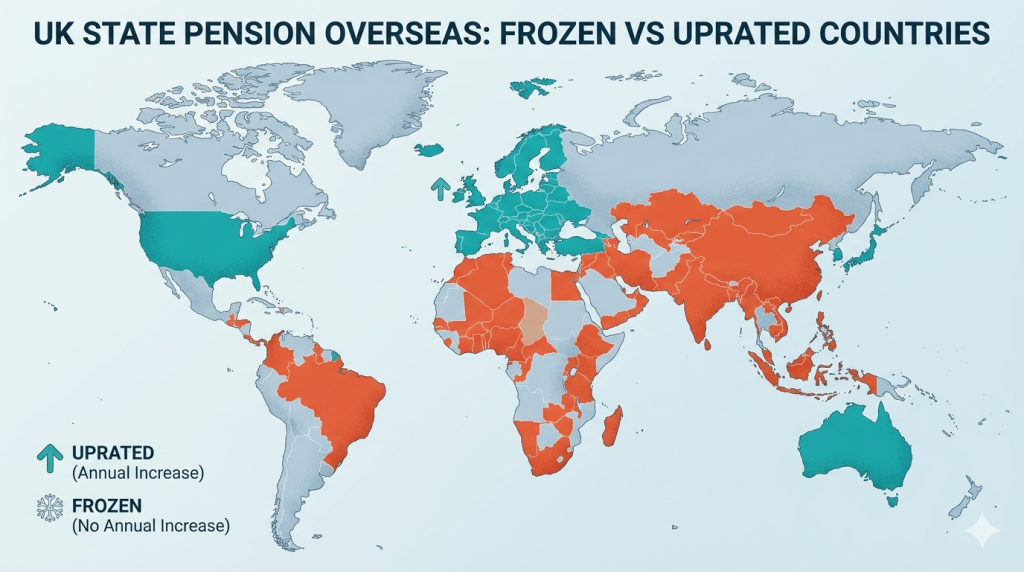

Truth 2: The Frozen Pension Scandal — Over 492,000 Pensioners Affected

This is where many people get a very nasty shock. While you can receive your uk state pension overseas in most countries, whether it increases each year depends entirely on where you live.

There are two groups:

- Uprated countries: If you live in the EU, EEA, Gibraltar, Switzerland, the USA, or countries with a reciprocal social security agreement, your pension increases each year in line with the Triple Lock — currently the higher of inflation, earnings growth, or 2.5%.

- Frozen pension countries: If you move to Australia, Canada, New Zealand, or many other countries, your pension is frozen at the rate it was when you first claimed it — or when you left the UK. It never increases, no matter how long you live there.

According to the House of Commons Library, as of May 2020, 492,176 people overseas were receiving a frozen UK State Pension — with 84% living in Australia, Canada, or New Zealand. The government has maintained this policy for over 70 years and has no plans to change it.

The financial impact over a retirement can be enormous. Someone who retired abroad in 2010 on £100 per week and lived in a frozen pension country would still be receiving £100 per week today — while a pensioner in Spain would be receiving considerably more after years of annual increases.

| ⚠️ Important Warning |

| Always check the frozen pension status of your intended country BEFORE you move. The government maintains a full list of countries and their uprating status at gov.uk/pension-credit/further-information. |

Truth 3: The 2026 NI Changes — Filling Pension Gaps Just Got a Lot More Expensive

This is the biggest change affecting expats right now. From 6 April 2026, the rules around voluntary National Insurance contributions for people living abroad changed dramatically — and if you have gaps in your NI record, it will now cost you significantly more to fill them.

Here is what changed:

- Before April 2026: Expats could pay Class 2 voluntary NI contributions at just £3.45 per week (approximately £182 per year) to build qualifying years towards their State Pension.

- From April 2026: Class 2 contributions for overseas residents have been abolished. Expats must now pay Class 3 contributions at £18.45 per week — approximately £960 per year.

That is an increase of over £778 per year — or more than £7,700 over a decade. The government’s stated reason is to ensure that people building a State Pension from abroad have a sufficient link to the UK and that the rate better reflects the value of the benefit received.

Additionally, from the 2026/27 tax year, you must now have lived in the UK for 10 consecutive years or made 10 years of UK-based NI payments to be eligible to make voluntary contributions at all — up from the previous requirement of just three years.

If you are approaching State Pension age and have gaps in your record, it is worth speaking to a financial adviser sooner rather than later. You can find regulated advisers through MoneyHelper.

Truth 4: Tax — You May Owe It in Two Countries

Receiving a uk state pension overseas does not automatically mean you stop paying UK tax. The State Pension counts as taxable income under UK rules. However, whether you actually pay UK tax depends on your residency status and the tax treaties between the UK and your new country.

Here is a simplified overview:

- If your total UK income exceeds your Personal Allowance (£12,570 in 2025/26), HMRC will collect tax owed — usually by adjusting your tax code on any workplace or private pension you receive.

- Many countries have double taxation agreements with the UK — meaning you will not pay tax twice on the same income. The USA, most EU countries, and many others have such agreements in place.

- Some countries have no agreement — in which case you may owe tax in both countries simultaneously.

Before moving abroad, always check the HMRC list of double taxation agreements and consider taking specialist expat financial advice. This is one area where getting it wrong can be very costly.

You may also want to read our article: Making a Will in Retirement — Why It Matters More Than You Think — especially relevant if you are moving overseas and want to protect your estate.

Truth 5: You Must Notify the DWP and HMRC Before You Move

This is the practical step most people overlook. Before you move abroad, you have legal obligations to notify both the Department for Work and Pensions (DWP) and HMRC. Failing to do so can result in overpayments, underpayments, and potential penalties.

Your pre-departure checklist:

- Contact the International Pension Centre to inform them of your move and provide your overseas bank account details. The International Pension Centre is your first port of call when claiming from outside the UK — they handle all overseas pension payments and can advise on your specific situation to claim.

- Notify HMRC of your change of residency — this affects your tax code and National Insurance status.

- Check your NI record for any gaps you may wish to fill before you leave — especially given the 2026 cost increases.

- Verify whether your destination country has a reciprocal agreement with the UK and whether your pension will be uprated or frozen.

- Inform your private or workplace pension provider of your new address and banking arrangements.

- Consider your NHS entitlement — you will generally lose access to free NHS treatment once you move abroad permanently.

Common Questions About Your UK State Pension Overseas

Can I claim my UK State Pension if I have never lived abroad before?

Yes — as long as you have the required qualifying National Insurance years, you can claim your State Pension wherever in the world you choose to live in retirement.

What happens if I move back to the UK?

If you previously had a frozen pension and move back to the UK, your pension will be unfrozen and will begin to increase again. However, you will not receive backdated increases for the years your pension was frozen.

Can my spouse or partner inherit my State Pension if I die abroad?

Potentially yes, depending on their own NI record and when you reached State Pension age. For full details, read our article: Can I Inherit My Husband’s State Pension?.

Is my workplace or private pension also affected?

Your workplace and private pensions remain yours when you move abroad and stay invested. However, your tax position and banking arrangements may change, and you may only access them from age 57 from 2028 onwards.

Does the UK state pension in Ireland get annual increases?

Yes — if you retire to Ireland your UK state pension in Ireland is uprated annually as Ireland is in the EEA, meaning you receive the full Triple Lock increases each year.

| 💡 The Honest Pensioner’s View |

| Retiring abroad can be a wonderful chapter in life — but your UK state pension overseas deserves serious thought before you commit. The frozen pension trap catches thousands of people off guard, and the 2026 NI changes mean the window for affordable top-ups has now closed for most expats. Take your time, do your research, and if in doubt — get professional advice from a regulated financial adviser who specialises in expat retirement planning. |

Have you moved abroad or are you thinking about it? We would love to hear your experience — leave a comment below and let us know how your UK state pension overseas has worked out for you. And if you found this article helpful, share it with someone who is planning their retirement abroad.