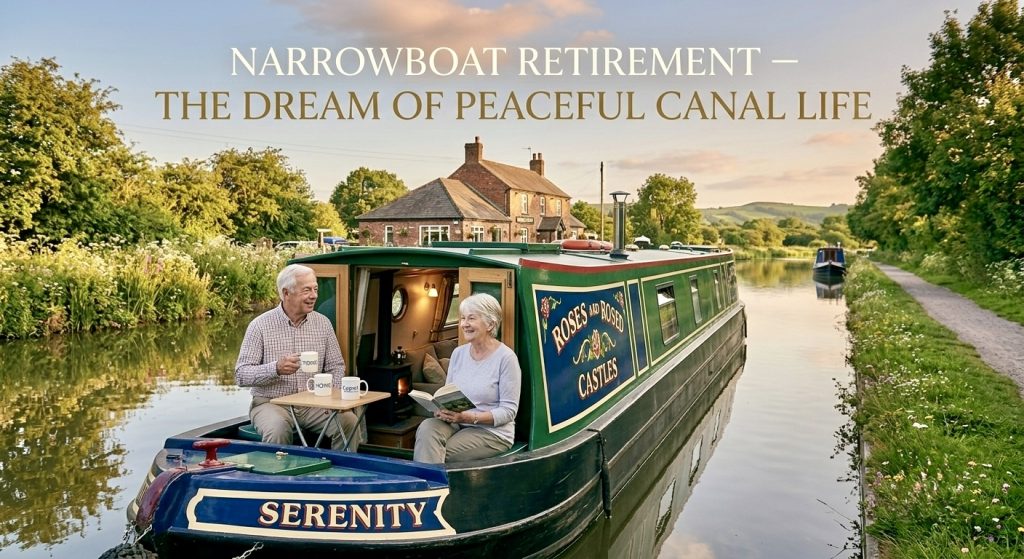

Narrowboat living in retirement has become a genuine dream for thousands of over-55s across the UK. The images are compelling — peaceful waterways, birdsong, lower bills and the freedom to move your home whenever the mood takes you. It sounds like the perfect way to make your money go further while finally enjoying life on your own terms.

But before you sell your family home and step aboard, it is worth reading our guide on thinking of downsizing your home — because there are 7 harsh truths about narrowboat living in retirement that most lifestyle articles conveniently ignore. This guide gives you the honest picture — the appeal, the risks, the financial trap, and the questions you must answer before you commit.

Table of Contents

Truth 1: The Appeal of Narrowboat Living in Retirement Is Very Real

Let us be clear from the outset — narrowboat living in retirement has genuine and compelling appeal. Thousands of retirees across the UK have made the move and never looked back.

As a continuous cruiser, moving every 14 days as required by the Canal and River Trust, you are generally exempt from council tax entirely. The UK has over 2,000 miles of connected canals and waterways — enough to spend years exploring without repeating a route.

There is also a strong sense of community on the waterways. Fellow liveaboards tend to be practical, friendly and self-sufficient — exactly the kind of neighbours that make retirement feel less isolating. Life on a canal boat slows down in the best possible way.

And the financial headline is hard to ignore. According to the Office for National Statistics UK House Price Index, the average UK house price is currently £270,000. Sell your home, buy a decent live-aboard narrowboat for £70,000 to £80,000, and you appear to have released a significant lump sum to support your retirement. The problem is what happens next.

Truth 2: Narrowboat Living in Retirement Comes With a Depreciation Trap

The Fundamental Financial Difference

A house bought today will almost certainly be worth more in five years. UK house prices have risen by 3.8% annually according to the latest ONS data. A narrowboat bought today will be worth less. Hull wear, engine age, weathering and general use all erode value over time.

This is the financial reality that lifestyle articles about narrowboat living in retirement rarely address. Property appreciates. Boats depreciate. That single difference can define whether your retirement plan works or unravels.

The Numbers That Matter

Here is what the financial picture actually looks like when considering a narrowboat in retirement:

- Sell average UK home: £270,000

- Buy a decent live-aboard narrowboat: £70,000 to £80,000

- Remaining capital after purchase and moving costs: approximately £175,000 to £185,000

- UK house prices rising at 3.8% annually — your original home could be worth £320,000+ in five years

- Your narrowboat over the same period will be worth less than you paid

- The gap between what you have left and what re-entry to the property market costs is the trap

That £175,000 to £185,000 sounds substantial. But draw on it over four or five years of canal life, add the ongoing running costs, and factor in house price growth — and re-entering the property market at anything like your previous standard becomes extremely difficult.

If you are already a homeowner wondering about your options, our guide to remortgage in retirement [INTERNAL LINK — hyperlink to: remortgage in retirement] covers the alternatives worth considering before you make any irreversible decisions.

House price growth figures are sourced from the ONS UK House Price Index April 2026

Truth 3: The Running Costs of Narrowboat Living in Retirement Are Higher Than People Expect

One of the most common misconceptions about a narrowboat in retirement is that it is simply cheap to run. It can be more affordable than a house — but the costs are real, ongoing and easy to underestimate.

Here is a realistic annual cost breakdown for narrowboat living in retirement:

- Canal and River Trust annual licence: approximately £1,100 for a 48ft narrowboat

- Residential mooring fees if not continuously cruising: £4,000 to £10,000+ per year

- Hull blacking — essential corrosion protection: £1,000 to £2,000 every 2 to 3 years

- Engine servicing, mechanical repairs and pump-outs

- Boat Safety Certificate renewal: approximately £200 every 4 years

- Insurance: £400 to £800 per year

- Diesel for heating and engine: variable but significant in winter

The estimated total annual running cost for narrowboat living in retirement ranges from £8,000 to £18,000 or more — before food, living expenses or any drawings from your capital pot.

Truth 4: Many Retirees Find a Marina and Never Move — Making Narrowboat Living in Retirement Expensive

A significant number of retirees who buy a canal boat with dreams of continuous cruising end up moored permanently in a residential marina within a year or two — and never leave.

Warning: living on a narrowboat in a residential marina is a very different financial proposition to the freedom-of-the-waterways dream. These owners are paying substantial monthly marina fees to live in a very small floating home with no garden, no driveway and no capital growth on their asset — while still bearing all the maintenance costs of boat ownership.

A narrowboat may be harder to sell than you expect, particularly from a static residential mooring. The second-hand narrowboat market can be thin. A boat that cost £75,000 may achieve considerably less when sold several years later.

Before committing to narrowboat living in retirement, ask yourself honestly: am I buying a boat to cruise — or am I buying a lifestyle I will actually live?

Truth 5: Bereavement Can Make Narrowboat Living in Retirement Unmanageable Overnight

Most people who choose narrowboat living in retirement do so as a couple. The lifestyle is designed for two — one on the tiller, one working the lock. The practicalities of canal life are far more manageable when you have a partner alongside you.

Losing that partner changes everything. Managing a narrowboat alone after bereavement is not just harder — it can be genuinely unsafe. Locks require sustained physical effort. Mooring in difficult conditions is a two-person task. Winter nights on the cut alone, far from family and friends, can be desperately isolating at a time when support matters most.

What worked beautifully as a couple can become untenable overnight — and the financial pressure of needing to sell the boat and re-enter the property market compounds an already devastating situation. Our article on common law partner rights after death is essential reading for unmarried couples considering this lifestyle together.

Truth 6: Illness and Ageing Make Narrowboat Living in Retirement Increasingly Difficult

When Serious Illness Strikes

A stroke, a serious fall, a cancer diagnosis or simply gradual physical decline can make canal life impractical almost overnight. Getting on and off a narrowboat requires balance and mobility. Managing the tiller, climbing steps from the towpath, operating lock gates — tasks that seemed manageable at 63 may become impossible at 73.

There is also a practical emergency concern that few people consider. If you need an ambulance urgently, your location on a rural canal towpath may significantly delay response times compared to a home address.

Cramped Conditions Become Harder as You Age

The compact interior that feels characterful and cosy in your early retirement years can become genuinely difficult as your body changes. There is typically no bath. Storage is limited. There is no space for a walking frame, a wheelchair or the mobility aids that become part of daily life for many people in their seventies.

The boat does not adapt as your needs change. That inflexibility is one of the most underappreciated risks of narrowboat living in retirement.

If health is a concern, it is worth reading our guide to care home fees and what to consider before you make any major property decision.

Our comparison of sheltered housing vs care home costs [INTERNAL LINK — hyperlink to: sheltered housing vs care home costs] is also worth reading if you are weighing up longer-term housing options.

Truth 7: Getting Back Into the Property Market After Narrowboat Living in Retirement Is Harder Than You Think

If any of the scenarios above forces you to exit narrowboat living in retirement — bereavement, illness, a change of heart, or simply growing older — you will need to re-enter the property market. And the market will not have waited for you.

UK house prices have been rising at 3.8% annually. The home you sold for £270,000 could be worth £320,000 or more five years later. Meanwhile your narrowboat has depreciated, your capital pot has been drawn down, and a distressed sale of a second-hand boat rarely achieves asking price.

The gap between what you have left and what you need to buy back into the property market is the real narrowboat retirement trap. Before selling, it is worth exploring whether renting a room in retirement could release income from your current home instead — without the irreversible step of selling it.

FAQ: What Are the Drawbacks of Narrowboat Living in Retirement?

The main drawbacks of narrowboat living in retirement are financial and practical. A narrowboat is a depreciating asset unlike property. Running costs of £8,000 to £18,000 per year can erode your capital quickly. Re-entering the property market after selling your home is difficult if house prices have risen in the interim.

On the practical side, the physical demands of canal life — locks, mooring, maintenance — become harder with age. Limited space, no bath, and restricted emergency access all add to the challenges. Isolation is a genuine risk, particularly for those who end up alone.

FAQ: How Much Does It Cost Per Year to Live on a Narrowboat in Retirement?

As a realistic annual guide for narrowboat living in retirement:

- CRT licence: £1,100

- Residential mooring if not continuously cruising: £4,000 to £10,000

- Diesel and fuel: £1,500 to £2,500

- Maintenance and repairs: £1,000 to £3,000

- Insurance: £400 to £800

- Pump-outs and water: £300 to £500

- Estimated total: £8,000 to £18,000+ per year

This is before food, living costs or any drawings from your capital. For many retirees the total cost of narrowboat living is higher than expected once all expenses are factored in.

FAQ: Do You Pay Council Tax When Living on a Narrowboat in Retirement?

If you are a continuous cruiser — moving every 14 days as required by the Canal and River Trust — you are generally not liable for council tax. This is one of the genuine financial advantages of narrowboat living in retirement.

If you have a permanent residential mooring however, the mooring site owner typically pays council tax and passes this cost on through your fees. For full details on mooring rules and licensing see the Canal and River Trust website .

FAQ: Can I Claim Benefits If I Live on a Narrowboat in Retirement?

Yes — in most cases. State Pension, Pension Credit and Universal Credit are generally available to those living on a narrowboat in retirement, provided you are registered with a local authority for correspondence purposes. Most liveaboards use their marina address or a registered mail address.

It is always worth checking your specific entitlements before making any decisions. Full guidance is available on the GOV.UK benefits pages

Before You Sell: A 7-Point Checklist for Narrowboat Living in Retirement

Narrowboat living in retirement can work brilliantly — but only if you have genuinely stress-tested the decision. Work through this checklist before you commit:

- Have you hired a narrowboat for at least 3 months across different seasons, including a full winter?

- Have you calculated what re-entering the property market would cost in 5 years at 3.8% annual house price growth?

- Do you have savings outside the boat purchase as a financial safety buffer?

- Have you taken independent financial advice on the equity gap risk?

- What is your plan if one of you becomes seriously ill, loses mobility or dies?

- Are you genuinely going to cruise continuously — or are you likely to find a marina and settle?

- Have you spent extended time alone on a narrowboat, not just as a couple on a holiday?

The Honest Verdict on Narrowboat Living in Retirement

Narrowboat living in retirement can be a genuinely wonderful and fulfilling chapter of life. The waterways are beautiful. The community is warm. The pace is healthy. And for the right person — fit, financially secure with capital to spare, comfortable with practical maintenance and genuinely committed to the cruising lifestyle — it can be an inspired retirement choice.

But for the majority of over-55s attracted to the idea, the financial risks are real and serious. Selling your family home and buying a depreciating asset that is difficult to exit deserves the same rigour you would apply to any major financial commitment.The dream is real. So is the trap. The difference between the two is the homework you do before you sell. If you are still weighing up your options, our guide on thinking of downsizing your home and our article on moving abroad in retirement moving abroad in retirement both cover the questions worth asking before making any irreversible retirement housing decision.